About Us

Trustees

Policyholders

Purposeful investments

Investors

New & insight

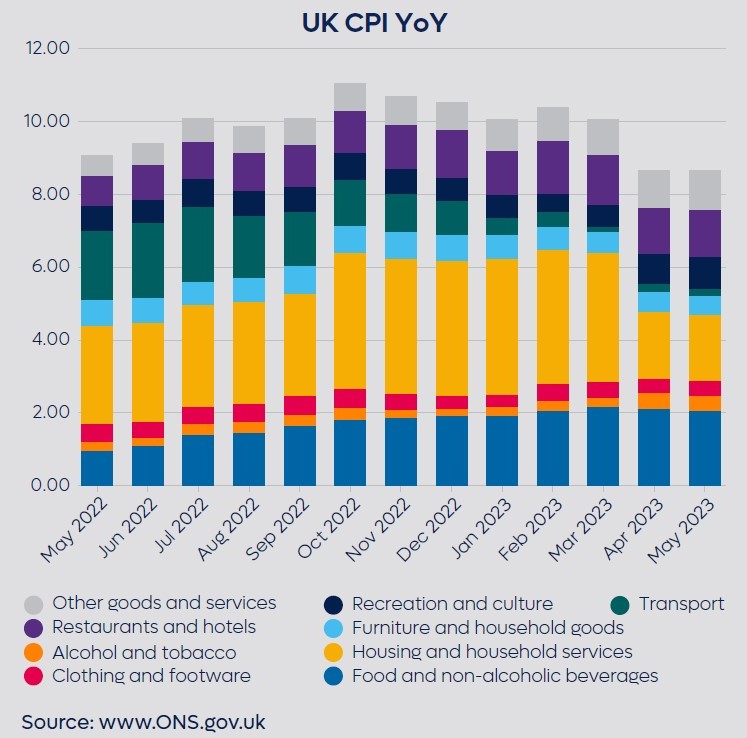

UK inflation is significantly and stubbornly above the Bank of England’s 2% target and May’s UK CPI (Consumer Price Index) was 8.7%, down from a peak of 11.1% in October.

News over recent months suggests food inflation and prices of other goods are starting to subside, but there is some evidence that the inflation of services like transport, phone bills, and the cost of leisure activities is ticking up at an increasing rate.

According to the Big Issue the recent price rises on food and utility bills impacted c.15% of the total bills facing a low income household, whereas it is c.10% of a high income household’s bills. The increased cost of living and reduced labour force has meant that many employees have lobbied for pay rises that meet or exceed inflation, hence the increase in collective bargaining and strikes. This impact on the lowest income groups is the reason that fighting inflation has become the driver of monetary policy.

According to the Monetary Policy Committee’s meeting notes on 21 June 2023 for the recent hike in rates to 5.0%: “The second-round effects in domestic price and wage developments generated by external cost shocks were likely to take longer to unwind than they had done to emerge”.

Higher rates have winners and losers. Inflation is a reduction in the purchasing power of your money. This impacts everyone, but mostly the less well off. Borrowers are also worse-off, affecting businesses, the government, and individuals alike. Individuals in the UK have mortgages as a significant portion of their total debt, and mortgage rates have increased notably. Mortgages are sensitive to the Bank of England’s Base Rate as borrowing tends to be for short periods in the UK between two and five years.

Savers are now better off, and this includes both individuals and savings institutions like pension funds, who are able to achieve a higher rate of return. Long term interest rates have edged higher not only because of higher inflation and interest rates but also because central banks who had been large buyers of government debt have halted their purchase programmes.

One question is: given the government is running a deficit, who will be the purchasers of government bonds? Overall yields are important in the pensions buyout market, as that drives the decisions for de-risking i.e., schemes reducing exposure to assets selected for growth and increasing exposure selected to match the pensions they need to pay out.